Personal Income Tax (PIT) in Myanmar

Htay Aung (Chris)

Easy PIT Calculations Link

Key Reference from IRD, VDB Loi and My experiences.

Personal Income Tax in Myanmar

When it comes to personal income tax (PIT) in Myanmar, both residents and non-residents are subject to tax obligations. Employers, whether they are resident or non-resident, are responsible for deducting PIT from payments made to their employees. This includes salaries and other types of emoluments. It is essential for employers to understand their responsibilities to ensure compliance with Myanmar's tax regulations.

Taxation of Residents and Non-Residents

Residents of Myanmar, including both local workers and foreigners living in the country, are taxed at a progressive rate on their worldwide income. This means that all income earned, regardless of its source, is subject to taxation. However, there are specified allowances and reliefs that residents can deduct, which may reduce their taxable income.

Foreigners who are not residents of Myanmar are taxed differently. They are only subject to tax on their Myanmar-sourced income. This distinction ensures that only income generated within Myanmar is taxed for non-residents, making it crucial to determine one's residency status for tax purposes.

Residency

A foreign individual is considered as a resident foreigner for tax purposes if they are residing in Myanmar for 183 days and more during an income year from 1 April 2023 to the following 31 March 2024 for FY2023-24 and 1 April 2024 to the following 31 March 2025 for FY2024-25. Accordingly, foreigners who are residing in Myanmar for less than 183 days are considered as non-resident foreigners.

Taxable salary

When it comes to taxable salary, understanding the various components that constitute it is essential for both employers and employees. According to the Income Tax Law (ITL), salary income includes various forms of compensation such as salary, wages, annuities, bonuses, awards, and fees or commissions received in lieu of or in addition to the salary or wages. This blog post aims to clarify what constitutes taxable salary and the implications for both parties involved.

Components of Taxable Salary

Salary income encompasses a wide range of compensations. Here are the key components:

Salary and Wages: The most obvious component, salary and wages are the regular payments received by an employee for their work. These amounts are fully taxable.

Annuities: Annuities are periodic payments made to an employee, often after retirement. These payments are taxable as they represent a form of deferred compensation.

Bonuses and Awards: Any bonuses or awards given to an employee are considered taxable income. These could be performance-related bonuses or awards for exceptional work.

Fees or Commissions: Fees or commissions received in lieu of or in addition to salary or wages are also taxable. This includes any extra payments an employee receives for services rendered.

The following types of incomes are exempt from PIT: pensions, gratuities, and money received from the state lottery. According to the UTL 2023 and UTL 2024 , anyone whose annual salary income is MMK4.8 million or less is exempt from paying PIT. According to the “Amended UTL 2023 and UTL 2024”, the personal income tax will be imposed on the income received by the non-resident Myanmar citizens in foreign countries. PIT payment must be made in the same foreign currency in which nonresident Myanmar citizens receive the income.

Tax reliefs and allowances

• Basic allowance of 20% of the total annual income, up to a maximum of MMK10,000,000 per year (approximately US$5,000)

• MMK1,000,000 (approximately US$500) per annum for one spouse who is not earning assessable income during a financial year and is living with the taxpayer

• MMK500,000 (approximately US$250) per annum for each child living with the taxpayer who fulfills ALL of the following criteria: (i) is unmarried; (ii) is not earning assessable income; and (iii) is either under 18, or if 18 or over, is in full-time education

• MMK1,000,000 (approximately US$500) per parent for dependent parents living with the taxpayer (the term “parent” includes a father- or mother-in-law)

• Premium paid for the life insurance of the taxpayer and the taxpayer’s spouse

• Contribution towards the savings fund as prescribed by the Income Tax Rules

• Social security contributions made by employees to the Social Security Board (2% of annual salary, capped at MMK72,000 per annum) (approximately US$36)

*Using an exchange rate of US$1 = MMK2,000

Rates of tax

The tax rates for resident and non-resident employees are now at the same progressive rates, although for resident taxpayers; the PIT rates are applied on their worldwide income after deduction of the reliefs and allowances above, while for non-resident foreigners; the PIT rates are applied on their Myanmar-sourced salary income without any deduction, and non-resident Myanmar citizens are liable to pay income tax on their salary income on the basis of two different calculation methods as follows,

Method 1 Subtract the tax relief (i.e., 20% basic allowance, parents’ allowance, dependent spouse and dependent child allowance, etc.,) from the total salary amount in accordance with Section 6 of ITL, calculate the income tax payable at the progressive personal income tax rate under Section 19 (c) of the UTL 2023 and UTL 2024 , and as per Clause 8 of the Income Tax Regulation (2018).

Method 2 Calculate the income tax on the total salary income at 2% without subtracting the tax relief under Section 6 and 6-A of the ITL.

Out of two tax amounts computed by Method 1 and Method 2 above, the lesser amount will be the PIT payable by a non-resident Myanmar citizen.

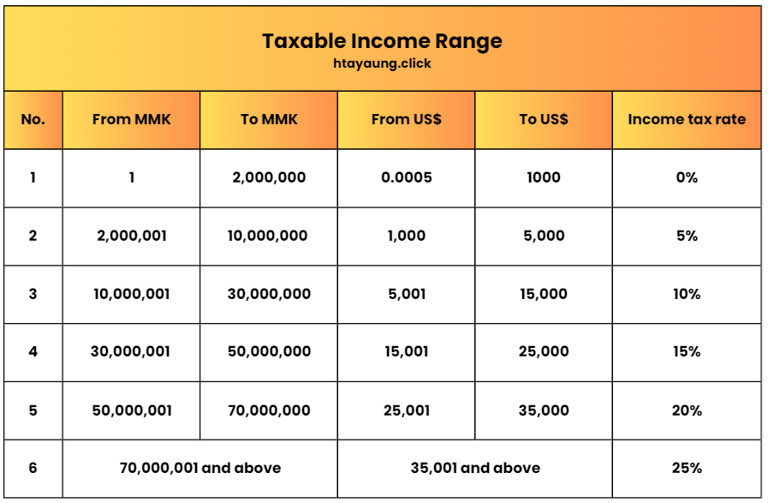

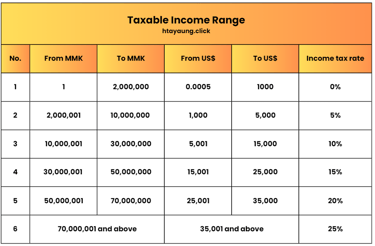

The following table shows the PIT rates on annual salary income. Approximate US$ amounts are shown in brackets based on an exchange rate of US$1 = MMK2,000.

Understanding the personal income tax system in Myanmar is essential for both individuals and employers. By staying informed about tax rates, allowances, and responsibilities, you can ensure compliance and potentially reduce your tax burden. Whether you are a resident or a non-resident, taking the time to understand your tax obligations will help you manage your financial affairs more effectively.